Vova's Blog

I write about machine learning and finance

Closed straddle strategy

by Vladimir

Now I can sum up the full result and analyze the effect.

The portfolio kept one and a half months and had 3 modifications:

- Initial formation of a call spread in the form of "straddle."

- At renewal of a trend closing of the left leg and transition to a long stake

- Change to a bull call spread.

I described the first two points in the previous post (here the reference: https://vk.com/wall-103610476_242? w=page-103610476_53705610). I will dwell on the last a little:

After the closing of the left leg (sale of fetters options), I had a clean equivalent of Long. Considering that I work with options, but not with the primary market, a sin was not to seize all additional opportunities to maximize income. And I made decisions to begin to sell stakes "out of money," thereby forming "a bull call spread."

Eventually, at me the call spread 15000-17250 turned out. In such look, the position came to expiration.

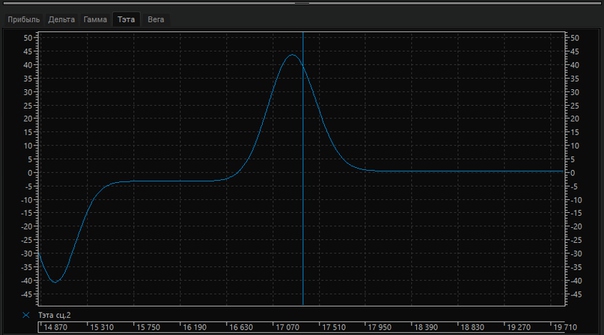

I will tell at once, the sale of the option I well "cut off" to myself profit as sold a stake too close to money in the growing market. Of course, it was covered with other option, but the current variation took away a lot of money when the price of the option began to grow with a growth of the price (At the market in 17350, the option sold by me became "on money", so its price grew as much as possible. Here schedule of a teta.

Apparently, the market was closed to its maximum values. And it left to me in kopek.

Morals: it is impossible to underestimate the force of a trend and to form very narrow spreads.

Anyway, I consider that I the idea well worked myself. Both options were executed and made profit on "a long position."

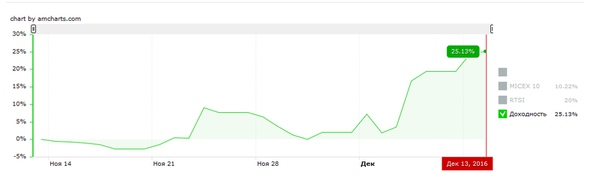

As a result, the profitability of all portfolio in 1.5 months made 25.13% that in itself is quite good.

I think that about new year I will leave work with options so far, it is too much another matters, plus it will be necessary to analyze all mistakes once again. All best!